TAA Consensus — April 2026

Energy hits overweight, the consensus jumps on a train that has already run 33%.

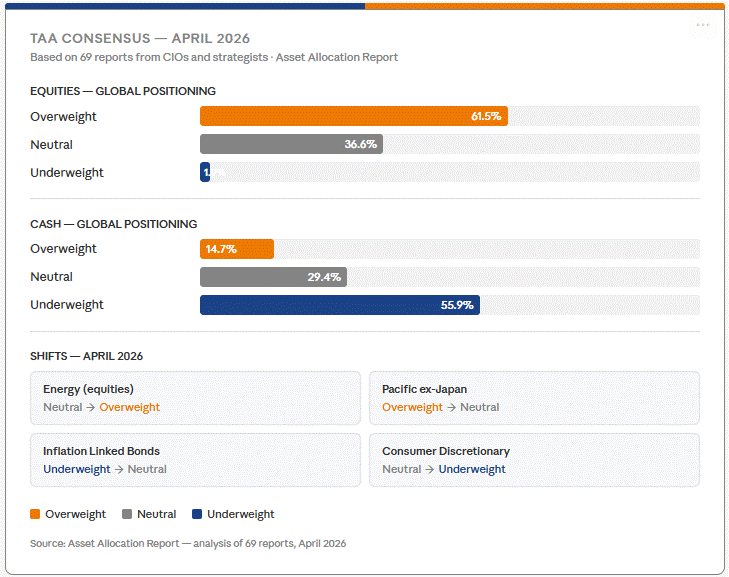

Heading into May, 61.5% of CIOs and strategists are overweight equities. Only 1.9% are not.

THE NARRATIVE

Four shifts dominate the April consensus. Pacific ex-Japan drops from overweight to neutral, the region has delivered what it needed to deliver. Inflation Linked Bonds move from underweight to neutral, driven by the inflationary pressure the energy shock brings with it. Consumer Discretionary falls to underweight: the consumer is holding back spending as long as energy prices remain elevated.

The most pronounced move is Energy. In March, the sector moved from underweight to neutral. In April, Energy stands at overweight, year-to-date return approximately +33%, in euros and dollars nearly identical. The sector is no longer as dominant as in previous cycles, but the direction is unmistakable: higher oil prices translate directly into higher revenues, and American energy producers combine that price advantage with lower transportation costs than Middle Eastern competitors. Dividends and buybacks at record levels further reinforce shareholder value creation. The classic dilemma for anyone who missed the move: the consensus is already riding momentum, but the de-escalation risk is real, a ceasefire and reopening of the Strait of Hormuz could trigger a sharp correction in energy prices.

Emerging Markets Equities remain the most attractive equity region without interruption, since July 2025, with two brief exceptions when the US was fractionally more attractive in November 2025 and February 2026. Historically, EM now sits in the top 5% of attractiveness over fourteen years. Emerging Market Debt has been the most attractive fixed income category since June 2025. The conversation with Valentijn van Nieuwenhuijzen on EM and EMD as the most attractive asset classes, conducted earlier this year, still holds. The data have only strengthened the case since.

The broad preference for equities rests on three pillars: AI-driven earnings growth spreading from technology into industrials, utilities and energy, with estimated S&P 500 earnings growth of 15–19% for 2026; a resilient US macro environment with a strong labour market and productivity gains; and broadening market leadership as equal-weight S&P 500 and small caps begin to close the gap on the Magnificent Seven. Valuations have pulled back from the 95th to the 73rd percentile after the correction: not a bargain, but no longer extreme either.

THE OTHER CAMP

Two structural risks deserve attention. The Shiller CAPE stands at approximately 32x, historically consistent with roughly 4% annual returns over ten years, regardless of what the quarterly earnings print says. At the same time, the correlation between equities and bonds has turned positive as a result of the energy shock: bonds are no longer fulfilling their role as a portfolio buffer at precisely the moment that matters most. J. Safra Sarasin goes a step further as a contrarian, standing underweight energy on the argument that the market has already priced in most of the good news and that risk/reward at current levels is unattractive.

WHAT TO WATCH

If the Strait of Hormuz reopens within three weeks, the narrative supporting Energy collapses, and the consensus direction may turn faster than the data currently suggest.

The train is moving, and 61.5% of CIOs are on board. Those still on the platform are weighing momentum against the one scenario that ends the journey abruptly: a ceasefire, a reopened Strait, an energy price that falls as fast as it rose. The consensus is right more often than not. But trains that have already travelled 33% rarely stop at the moment everyone decides to board.

New to this? Energy stocks are rising because a blocked shipping route in the Middle East is pushing up the oil price, and higher oil prices mean higher profits for energy companies. The question dividing 69 reports this month: is this the beginning of a longer ride, or the final stop?