Interview | Valentijn van Nieuwenhuijzen on Emerging Markets

Why 60+ asset managers prefer EM, despite FX, China, and tariff risks

For this interview, I sat down with Valentijn van Nieuwenhuijzen, author of the Substack Always Expect the Unexpected. Valentijn brings 25+ years of experience from senior roles at Goldman Sachs Asset Management, NN Investment Partners and ING Investment Management, spanning macro, multi-asset investing, portfolio construction and sustainability.

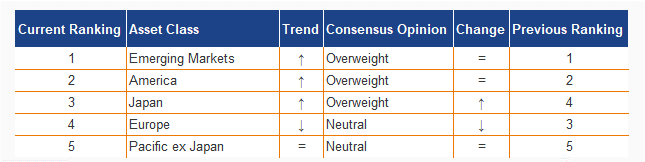

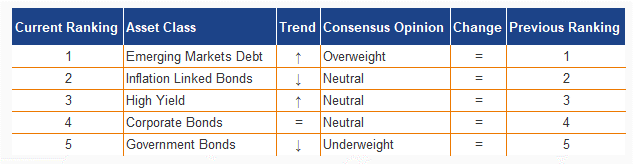

Our conversation builds on insights from the latest Asset Allocation Report by Alpha Research, which synthesises the tactical views of 60+ global asset managers. One result is particularly striking: Emerging Markets currently rank as the most attractive asset class across both equities and bonds, a rare combination.

In this interview, we work through the key building blocks behind this renewed EM tilt: what had to align for it to show up in both equities and bonds, why valuation supports the case but rarely times the entry, and how the USD, liquidity and flows can turn a strong thesis into a fragile trade.

Valentijn also shares his own reflections on the discussion on Always Expect the Unexpected, a great companion read to this piece.

Below, the full conversation is structured in 16 questions, moving from the “why now” signals to the practical portfolio questions: where EM is most vulnerable, what could change the view, and how to implement without turning it into one big EM bet.

1) The striking consensus

Eelco: What stood out to you when you saw that Emerging Markets came out as the most attractive asset class for both equities and bonds?

Valentijn: I found that very striking, because Emerging Markets have been somewhat out of favour with both institutional and retail investors in recent years. A strong dollar, weak commodity prices, rising interest rates in developed markets, and long-standing disappointments around corporate profitability in EM all created headwinds until about a year ago. That picture clearly started to turn over the course of 2025.

Why is this combination so rare right now, and what had to ‘come together’ for this outcome?

What really stands out to me is that EM equities have also become more popular again. EM debt has long been a structural overweight for many institutional investors, with a solid track record of delivering extra return and diversification in fixed-income portfolios. That has never really been the case for EM equities. Over the past 20 years, the asset class has largely failed to deliver on its promise. Despite higher economic growth in these regions, it has rarely translated into superior earnings growth or higher returns on equity than in the developed world.

2) What is the real driver: macro, valuation, or the USD?

Eelco: If you had to pick one factor pulling EM today - valuation, the USD, or financial conditions - which would it be?

Valentijn: If I really have to pick one factor, it wouldn’t be any of the three you mention. I would point instead to the broader search among investors for new sources of growth and return outside the US, triggered by Trump’s policy agenda.

What are the two signals that would make you say: ‘okay, this factor is now turning against EM’?

Many emerging markets are highly dependent on global trade. The trade restrictions and tariffs currently being rolled out by the US pose both direct and indirect risks, especially if other countries follow suit. That creates clear headwinds for EM.

3) Valuations: cheap, but cheap is not enough

Eelco: Many asset managers point to attractive valuations. When is ‘cheap’ a real buy signal for EM?

Valentijn: Cheap sounds attractive, but it is rarely a good entry signal. Often there are very good reasons, like structural problems, why assets are cheap. And just as often, markets are willing to keep buying “expensive” assets far longer than seems rational. For me, valuation is a supportive long-term argument, but almost never a trigger to enter a position.

Which valuation metric do you find most useful: P/E, P/B, risk premium versus DM, or something else?

There is no universal rule. It differs by asset class and by whether you are looking at equities, bonds, or commodities. Risk premia are probably the best metric for comparing asset classes, but even that breaks down for commodities, which generate no earnings or cash flows and therefore can’t be assessed using most traditional valuation measures.

4) The USD as a pivot point

Eelco: How important is USD stabilisation or weakness in your EM case?

Valentijn: The USD plays a major role. EM performance has always been highly sensitive to capital flows, across equities, debt, and FX. That sensitivity may be even greater now, because after years of US return exceptionalism, investors are genuinely searching for alternative sources of return. The USD weakened sharply in the first half of last year and is under pressure again this year, which clearly coincides with strong EM performance.

If the USD strengthens again, which EM segments are most resilient and which are most vulnerable?

So far, the weakest parts of EM have been China and then India. That’s striking, given they are by far the largest EM economies and therefore key focal points for the Trump administration. Escalating trade tensions with the US could weigh disproportionately on them. China also faces major domestic challenges, deflation, a housing market correction, and so on.

If the USD were to strengthen again, however, I would expect the most negative impact in EM segments that are highly dependent on capital flows, smaller economies in Southeast Asia, Latin America, and Africa.

5) Financial conditions and risk appetite

Eelco: Many analyses link EM performance to looser financial and monetary conditions. How does that transmission work in practice?

Valentijn: That ties directly back to EM’s sensitivity to capital flows. When financial conditions are loose and global risk appetite is high, capital flows toward riskier parts of the world. EM clearly falls into that category. These psychologically driven capital flows often dominate fundamentals, although the two can of course reinforce each other.

What do you actually watch: global liquidity, credit spreads, PMIs, central bank expectations, or flows?

You never look at just one indicator. Many of these variables are interconnected. Global liquidity is always a function of both the cost of credit - set by central banks like the Fed - and the willingness to use leverage, whether in corporate balance sheets or investment strategies such as hedge funds, leveraged ETFs, or private equity. Fed and ECB expectations, observed flows, and market-priced credit spreads each describe part of the broader liquidity and risk-appetite story.

6) China: the biggest source of noise, or still the key catalyst?

Eelco: In the bear case, China and tech weakness keep coming back. Is China still the EM factor for you?

Valentijn: China has clearly lost some relative importance for the EM region because of other supportive factors, but it remains crucial. Trade between China and the rest of EM is enormous and still growing. If China were to weaken significantly, that would eventually weigh more heavily on the rest of EM. The good news is that this sensitivity appears to be declining, and China is currently growing at a modest, but relatively stable pace.

If you take China out of the picture, which EM story still stands - India, LatAm, EM EMEA, ASEAN - and why?

ASEAN and India clearly have the strongest growth potential, driven by growing populations and high nominal GDP growth prospects. Politically, this part of Asia is relatively stable and benefits from comparatively well-functioning institutions. Other EM regions generally face lower growth potential and more political or institutional instability.

7) Trade tensions and tariffs: headlines or fundamentals?

Eelco: How do you assess trade tensions and tariff risks, mostly sentiment and headlines, or structurally damaging to margins and earnings?

Valentijn: There are many layers to this. At the core, Trump’s tariff policy undeniably creates structural uncertainty around economic policy. As long as he is in power, that uncertainty will periodically catch markets off guard. Trade with the US will become more difficult for almost everyone, negatively affecting margins and earnings growth.

The key question is: how much? At the same time, new trade routes are being explored and new trade agreements are being signed between other regions. That will at least partially offset the loss of frictionless trade with the US and reinforces the idea that future growth opportunities may increasingly lie outside the US.

Which EM regions or sectors are most exposed and where do you see potential beneficiaries?

China is actually a more important trading partner for EM than the US. It imports large amounts of agricultural products and commodities from other EM countries, especially in Latin America, while much of its technology and manufactured goods trade is concentrated within Asia. If China were to re-accelerate meaningfully, that could provide a major additional boost to the rest of EM.

8) EM equity: earnings breadth beyond the US

Eelco: There is an argument that growth and earnings breadth outside the US are improving. Do you see that and where?

Valentijn: Yes, that is happening, but with an important caveat. Technology and financials are the largest earnings-growth sectors globally. In many EM countries, banks and the broader financial sector play a role, but tech exposure is far more uneven. The US still dominates global tech and therefore retains a large share of global earnings growth. China is trying to challenge this, but mainly succeeds domestically, leaving US tech dominance in the rest of the World largely intact.

Is this a cyclical rotation, or a multi-year trend?

The broadening of earnings growth beyond the US is a structural trend. But the tech dimension remains crucial. A true acceleration will only occur once tech winners outside the US emerge, whether in EM, Europe, Japan, or Korea.

9) EM debt: carry is attractive, but what’s the risk?

Eelco: With EM debt, the story is often yield and carry. What is the ‘hidden cost’ of that carry?

Valentijn: There is no hidden cost if you recognise that yield or carry is simply a risk premium. It’s the compensation you receive for providing capital to an EM government or company. The higher the risk, the higher the yield. The hidden cost only appears if you expect that extra return without bearing the underlying risk.

Where does that cost usually show up - FX, drawdowns in risk-off, liquidity, or politics?

Those risks certainly exist. FX risk is the largest issue for local-currency debt and EM equities, while liquidity is a major risk across all EM assets. Political risk at the global level mostly comes from Trump and the Fed, given their impact on liquidity conditions. Local political risk exists too, but can largely be diversified away across countries.

10) Hard currency versus local currency

Eelco: If you had to choose today: hard currency or local currency EM debt and why?

Valentijn: Very clearly hard-currency EM debt. Historically, the performance difference has strongly favoured hard currency. In theory that gap should be smaller, but persistent EM currency underperformance versus DM currencies has meant that local-currency debt delivers diversification but also much higher volatility and structurally lower returns.

What macro development would make you switch?

A combination of credible policy frameworks across EM and clear evidence that EM currencies have entered a sustained upward trend versus DM currencies.

11) Spreads, flows, and positioning

Eelco: How important are flows and positioning in your EM decisions?

Valentijn: Very important. Behavioural analysis and psychology should be core tools for modern investors. If you want to understand market dynamics and actively manage entry points and outperformance, you have to incorporate these elements. Flow and positioning data help identify inflection points and areas of fragility, which often determine the size of drawdowns during unexpected risk-off shocks.

What would you consider an ‘overcrowded’ signal?

Broad signs of excessive optimism among professional and retail investors. There are many indicators: surveys, positioning data, volatility pricing, and AI-based sentiment analysis from media, research, and earnings calls. Asset-class-specific indicators also matter, and this is often where investors can really differentiate themselves.

12) Risks: politics, FX, and regulation - how do you actually manage them?

Eelco: EM is often framed as ‘political risk, FX risk, volatility’. How do you translate that into concrete risk limits?

Valentijn: It’s not fundamentally different from other asset classes. There is now ample historical data for EM equities, EM hard-currency debt, and EM local-currency debt to estimate correlations, volatility, drawdowns, and expected returns. That allows you to determine appropriate portfolio weights. Risk is ultimately a source of return, also in EM, but you need a solid analytical framework to understand the uncertainty that can never be fully modelled.

Do you use hedges, country caps, drawdown rules — or mainly diversification?

FX hedging has historically made sense, which is one reason EM hard-currency debt has performed so well. Beyond that, hedges, caps, and drawdown controls all matter, but the right mix depends heavily on portfolio specifics and whether you are dealing with EM equity, hard-currency debt, local-currency debt, or a combination.

13) Implementation: making EM portfolio-proof

Eelco: “If you’re constructive on EM equities and debt, how do you avoid it becoming one big EM bet?”

Valentijn: It starts with a reality check. Correlations within EM are high, especially in stress periods, so drawdown management is critical. You need to stay acutely aware of exposure to Fed policy, liquidity, and risk appetite. Allocating to more resilient EM segments helps. Exposure to precious metals and oil producers can provide some protection in stress scenarios. Over time, large economies like China and India may also become more domestically driven, improving diversification across Em assets.

Do you use target bands, phasing, or sequence debt before equity?

Short answer: no. Start with your optimal EM portfolio and stay adaptive. As Keynes said, “When the facts change, I change my mind.” That principle applies to EM just as much as to developed markets, perhaps even more so.

14) Scenarios: when are you right, and when not?

Eelco: What’s your base-case scenario in which EM surprises over the next 6–12 months?

Valentijn: A modest acceleration in global growth driven by fiscal and monetary stimulus in developed markets, combined with slightly less tariff chaos from Trump as he shifts focus to domestic politics ahead of the midterms. That would channel capital toward EM in the search for above-average growth and returns. Positioning is tactically overweight, but strategically still underweight among large institutions. So, there is still ample room for further inflows.

And what’s the scenario where you have to admit: ‘this isn’t working’?

A US recession. That would accelerate Fed easing but also amplify Trump’s policy chaos and sharply increase global risk aversion. Capital would exit EM and move toward the few remaining safe havens — gold, German Bunds, and the Swiss franc.

15) What would change your mind?

Eelco: Which two or three datapoints would push you from overweight EM to neutral or underweight?

Valentijn: Strongly negative US employment data, a collapse of the AI capex boom, or a US invasion of Greenland.

And what would make you more aggressive?

A strong rebound in China’s domestic growth, or another wave of new trade agreements among EM regions themselves or with Europe, the UK, Japan, and Canada.

16) Closing question: the 30-second pitch

Eelco: If you had to pitch this to an investment committee in 30 seconds: why is EM attractive in both equity and debt right now?

Valentijn: In a rapidly changing and ageing world, the search for new sources of growth and return is more urgent than ever. Emerging Markets offer renewed potential on both fronts and stand to benefit from deeper partnerships with parts of the developed world that are actively seeking alternatives to the US. The global energy transition also creates opportunities, both through commodity trade and by enabling EM economies to leapfrog directly to cleaner, more productive energy systems. For large parts of Asia, Africa, and Latin America, this represents a development opportunity Europe and the US never had.

And what’s the one sentence you must add to frame the risk honestly?

In periods of stress, correlations between all EM assets converge toward one. Don’t overestimate diversification benefits when they matter most!

Eelco: Thank you, Valentijn. This was a very valuable discussion, and it genuinely helped sharpen how I think about the signals in the Asset Allocation Report.

Readers interested in the broader data behind this conversation can find the full Asset Allocation Report on my Substack. Valentijn’s own reflections are published on Always Expect the Unexpected.

Valentijn: It was my pleasure. I really enjoyed the conversation, thank you for sharing the insights from the report, and for the great dialogue on EM assets.

Really insightful interview. The point about correlation converging to one during stress is critical and gets overlooked too often when peopel build diversified EM exposure. I've seen this play out multiple times where carefully structured regional allocations collapse into beta in selloffs.