Sell in May still exists — not in markets, but in the minds of strategists

Twelve years of Asset Allocation Consensus data show that strategists and CIOs follow the "Sell in May" pattern without saying so out loud. Behaviour reveals what reports conceal.

The signal

69 strategists and CIOs weighed in on global equities in April: 61.5% are overweight, 1.9% underweight. The net score stands at 0.596, the lowest reading of 2026.

No strategist writes in their report:

I am selling in May because that is simply what one does. Yet they do it, on average, year after year.

Markets have no seasons, but the people who comment on them clearly do. On average, strategists and CIOs follow the “Sell in May” narrative, not as a conscious decision, but as a behavioural pattern that becomes visible across twelve years of data.

The consensus on global equities fell from 0.62 in January to 0.596 in April 2026: a consistent downward move, timed precisely toward the moment the adage says to step aside. No freefall, but the direction is unmistakable. And the timing is striking.

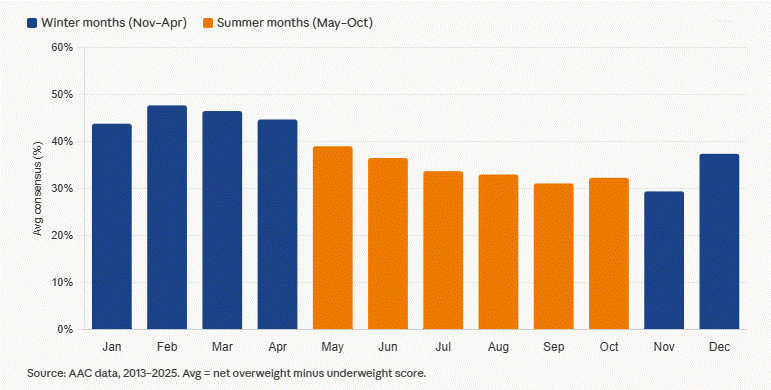

Our Asset Allocation Consensus (AAC) data over 2013–2025 make the pattern visible: optimism on global equities declines consistently from 43.8% in January to a low of 29.4% in November, a drop of nearly 14 percentage points across the year. The summer half-year averages 34.3%, the winter half-year 38.3%. Four percentage points, modest but consistent across twelve years.

Academic literature supports the effect. A study by Zhang and Jacobsen, published in the Journal of International Money and Finance (2021), analysed 62,962 monthly observations spanning 323 years and found that November through April outperforms May through October by an average of 4 percentage points, visible in 89 of 114 countries. What the AAC data add is a different dimension: not only does the market follow this pattern, so do the people whose job it is to interpret it. The analysis was conducted on global equities, measured via the MSCI ACWI Index.

But the classic adage cracks at one point. “Come back on Halloween” assumes November is strong. The data do not support that: November averages 0.294, the weakest month of the entire year, lower than every summer month except August and September. The winter half-year is carried by December, January and February. Not by November.

The other camp

One asset manager moved in the opposite direction in April: VP Bank upgraded from underweight to neutral, as shown in Our View in April dated 14 April 2026. That is not a wave, but it is the only contrarian signal in a dataset of 69 reports. Those who see the summers of 2024 and 2025 as counter-evidence, global equities rose 11% and 23.5% respectively in those periods, will find a fellow traveller in VP Bank. One voice, but a deliberate one.

What to watch

If the consensus score falls further in May and global equities nonetheless close positive, the behavioural pattern of strategists and the market outcome will have definitively parted ways. The effect would be more psychology than signal. The same analysis applied to US or European equities will follow if there is sufficient interest: let us know in the comments.

No strategist writes it down. No report concludes: we are turning cautious because May is approaching. But the data write it down, twelve years running, month after month, consistent and collective. “Sell in May” may no longer be a market effect. It is a mirror effect: markets behave as strategists expect, and strategists expect what they have always expected. To understand markets, you first need to understand the people who interpret them.

New to this? Global equities means listed companies from all major markets combined, and every month we measure how many professional investors want more or less exposure to them. If that number falls in May, the question becomes: are they responding to facts, or to an old saying?