Risk-on with a finger on the trigger

No allocator says they're positioned defensively. The positions tell a different story. Based on the Alpha Research Asset Allocation Consensus Premium, April 2026

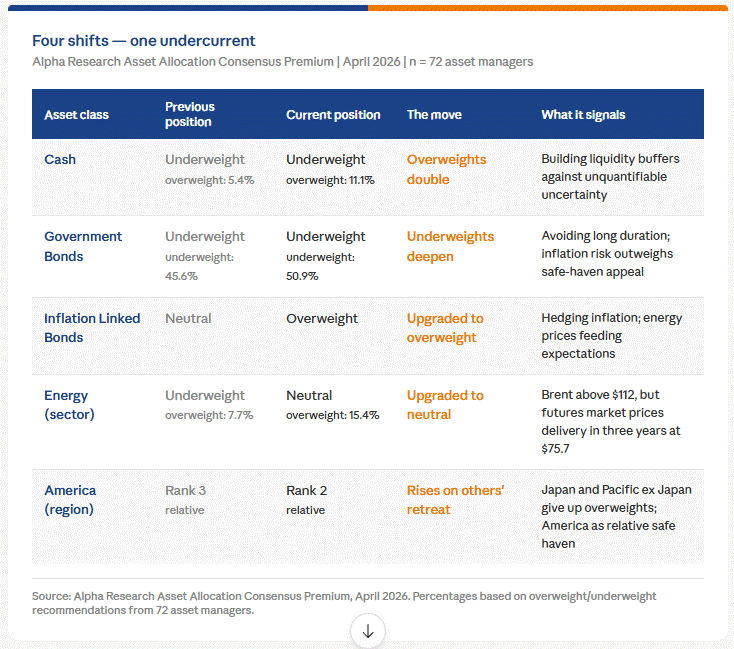

The consensus of 72 asset managers remains broadly constructive. Equities are overweight, bonds underweight, and overall positioning still points toward growth. But beneath that stable surface, four signals are shifting simultaneously, and they all point in the same direction.

Cash as an early warning system

The most striking signal is not in what is being overweighted, but in what is quietly being built up. Cash positions are recovering sharply: the percentage of overweight positions doubles from 5.4% to 11.1%, while underweights decline from 54.1% to 50.0%. Cash remains formally the least popular asset class. But the move is unmistakable. A growing group of allocators is building liquidity buffers, not as a strategic choice, but as protection against uncertainty they cannot quantify.

Avoiding duration, hedging inflation

That uncertainty has a name: inflation. Within fixed income, Inflation Linked Bonds shift from neutral to overweight, while Government Bonds slide further. More than half of all asset managers, 50.9%, are now underweight government bonds. The reasoning is sharp: higher energy prices driven by geopolitical tensions fuel inflation expectations, forcing central banks into caution and delaying rate cuts. Long duration becomes a risk, not a buffer. Spreads over duration: that is the implicit choice embedded in this consensus.

Energy: the market doesn’t believe its own prices

Brent is above $112. The energy sector rose +12.54% in March and stands at +40.94% year-to-date in euros. Yet Energy shifts only from underweight to neutral in sector allocation. The explanation lies in the futures market: one-year forward delivery prices $94.8, three-year forward prices $75.7. The market expects current energy prices to be temporary, and the consensus follows that judgment. Betting heavily on energy now means betting against the forward curve.

America wins by standing still

The fourth shift is the quietest. America climbs from third to second in regional equity allocation, not because conviction on America increases, but because Japan and Pacific ex Japan give up overweight positions. Emerging Markets retains its lead with 63.6% overweight recommendations, but America benefits as a relative safe haven: less exposed to the oil shock, less vulnerable to the geopolitical turbulence hitting Asia and Europe harder.

One theme, four moves

Four signals, one conclusion: the consensus repositions without changing course. Equities remain the core, but the edges are being reinforced. Cash up. Duration out. Inflation hedged. Energy normalised. The portfolios still run on growth, but the hands are moving toward the emergency brake.

New to this? Large asset managers adjust their portfolios monthly based on what they expect markets to do, these four shifts signal that professionals worldwide are quietly getting more cautious, even if they’re not saying so yet.