Four Asset Managers Read the Same Data. Only One Touched Credit.

Brent is up 58%. Credit spreads have barely moved. One of those numbers is wrong.

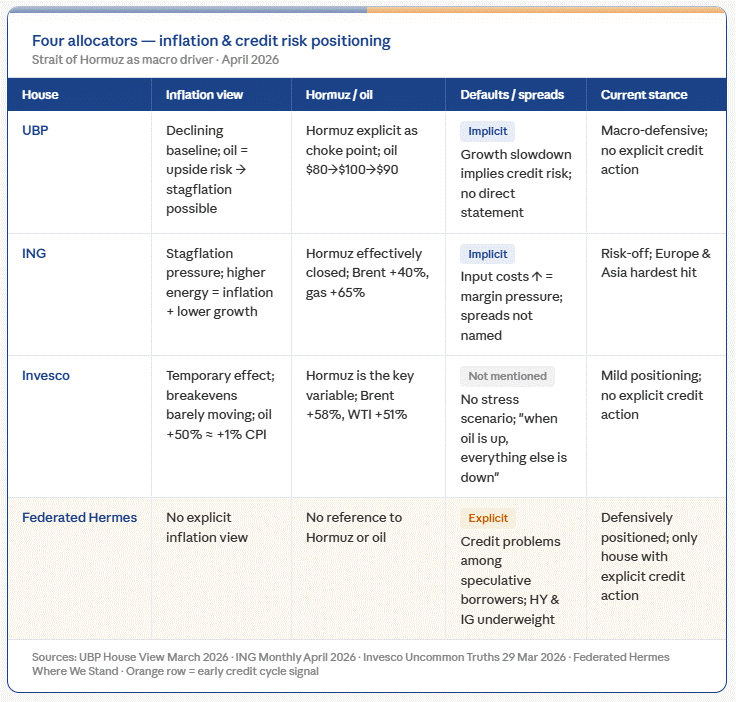

Four of the most successful asset managers in the world, selected through eleven editions of the Asset Allocation Awards on the basis of their ex-ante positioning over a rolling 36-month period, agree on one thing: the Strait of Hormuz is the single most important macro variable of this moment. Where they diverge is on what comes next, and that divergence may be more telling than the consensus itself.

Hormuz as transmission mechanism

The Strait handles roughly 20% of global energy flows. Since late February, Brent crude has risen 58% and natural gas 65%. The immediate market response was mechanical: risk-off positioning, hard hits to European and Asian equities, and a sharp repricing of energy-intensive sectors.

The inflationary arithmetic is well established. UBP, winner of both the Asset Allocation Award and the Overall Award at the 11th Asset Allocation Awards, lays out the transmission in their March 2026 House View: a $10 oil move adds between 0.2 and 0.5 percentage points to inflation, and oil at $100 per barrel translates to approximately 1.4 additional percentage points. The growth side mirrors it: a 10% energy increase reduces output by around 0.35 percentage points, and oil at $100 shaves a full percentage point from growth.

That combination — inflation up, growth down — is the textbook definition of stagflation.

Where the consensus splits

The inflation outlook divides the field. Invesco, winner of the Equities Sectors Award and the asset manager most attuned to cross-asset transmission, argues in their March 2026 edition of Uncommon Truths that the shock is temporary. Historically, a 50% oil rise adds roughly one percentage point to CPI, and breakeven inflation expectations have barely moved, suggesting markets are not yet pricing in structural damage.

ING Investment Office, winner of the Equities Regional Award, takes a harder line in their April 2026 Monthly. That regional discipline shapes their Hormuz analysis directly. In a year when virtually every major allocator tilted toward the US, ING explicitly chose neutral on North America at two quarterly junctures. That same discipline now plays out in their energy read: Brent +40%, gas +65%, Europe and Asia hardest hit, sector by sector. Their stagflation framing is not abstract. It is regionally grounded.

UBP and ING agree: the stagflation risk is real and not automatically self-correcting. The key variable for both is whether Hormuz reopens. If it does not, Invesco’s temporary thesis collapses.

The credit blind spot

Here is what the inflation debate obscures. None of these three asset managers, with one exception, has translated the macro deterioration into explicit credit risk. The stagflation scenario implies lower growth, compressed margins, and rising input costs for leveraged companies. The logical endpoint is wider spreads and higher defaults. Yet that step is largely absent from the analysis.

Federated Hermes is the exception. It is no coincidence that they won the Fixed Income Award at the 11th Asset Allocation Awards, in a year when the rate environment showed more movement than the preceding three years combined. Their March 2026 edition of Where We Stand is already defensively positioned: underweight both high yield and investment grade, with an explicit flag on credit problems among speculative borrowers. That is not scenario analysis. That is a position.

In a credit cycle, the distance between diagnosing and positioning is rarely academic. The three asset managers that built the stagflation case most precisely are now the asset managers slowest to act on its credit implications. Federated did not build a framework. Federated acted. When the credit cycle turns, that timing advantage will not be subtle.

The market remains in the early phase of a credit cycle that has not yet turned. Spreads are technically tight. Default rates are not yet rising. But the conditions that precede credit deterioration are accumulating. Stagflation, margin pressure, and reduced earnings visibility are the three variables that historically precede a turn. Invesco’s counterweight, stable breakeven expectations, suggests systemic stress has not arrived. If Federated’s positioning proves premature, that signal will move first.

The question allocators should be asking

The Strait of Hormuz is the ignition point. Oil is the transmission mechanism. Equities have repriced. The question that remains underpriced is whether this macro shock runs long enough and deep enough to produce the credit cycle that current spread levels do not yet reflect. That is not a macro question. It is a positioning question.

Four asset managers read the same data. Only one acted on all of it.

This analysis is based on the March 2026 editions of each publication. Updated positioning from all four asset managers with April data will be incorporated in our May 1st review.

New to this? The Strait of Hormuz is a narrow waterway in the Middle East through which one-fifth of the world’s oil passes, and right now it is largely closed, which means higher energy prices, slower growth, and rising pressure on company finances across your portfolio.