EM is a double favorite: Conviction, or a hidden USD bet?

68 TAA reports: EM leads equities and debt, across about €63tn in AUM.

This month’s question

Imagine markets occasionally forming a rare, coherent sentence. Not separate words, but one thought. What does it mean when Emerging Markets sit at the top in both equities and bonds? Is it coincidence, two separate league tables where EM simply offers the best risk/return? Or does it reveal something bigger, one overarching worldview in which the same wind pushes EM equities and EM debt at the same time? And if there is one variable that can connect these two worlds, are we, ultimately, looking into the same mirror, the US dollar?

One regime, two outcomes: EM equities and EMD

When EM Equities and EM Debt rank at the top simultaneously, it’s rarely a coincidence or two unrelated preferences. It usually signals one shared macro view, the wind has turned more favorable for EM. The core is a combination of a dollar that doesn’t strengthen, easier financial conditions, and broader growth and earnings beyond the US, forces that can lift EM equity valuations and earnings leverage while also supporting EMD via carry and spreads. The mirror image matters just as much, if the dollar rises, US rates surprise, or risk-off returns, both EM markets often get hit at the same time. In short, one regime, two outcomes, and that’s exactly what makes this double EM-favorite so telling.

At a glance

Dataset: 68 tactical asset-allocation reports

AUM covered: about €63tn

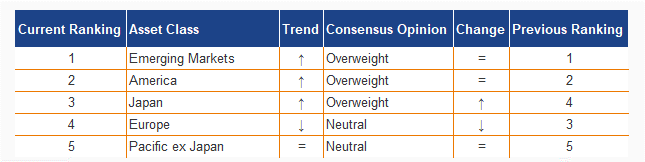

EM Equities: 53.1% overweight, 40.6% neutral, 6.3% underweight

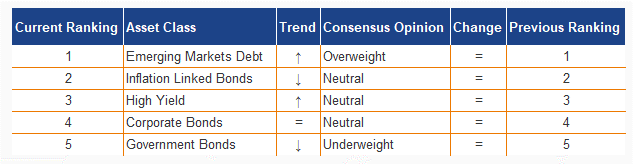

EM Debt (EMD): 53.7% overweight, 35.2% neutral, 11.1% underweight

Method note (Alpha Research): The bull and bear cases below are not my personal forecasts. They are a consensus synthesis based on reading 68 tactical asset-allocation reports. I’ve distilled the most frequently cited arguments and the key points of disagreement into a single, comparable framework, so you can see what the market’s strategists are collectively emphasizing right now.

68 reports, €63tn AUM: EM at the top

Table 1: Equities Regional Allocation

Table 2: Fixed Income Allocation

The “double-OW” reads: 13 reports behind EM #1

Within the full set of 68 tactical asset-allocation reports, 13 stand out, they place both EM Equities and EM Debt in overweight. These are the most useful reads if you want the full rationale, how each asset manager frames the dollar, financial conditions, carry, spreads, and the broader regime that makes EM number one across equities and fixed income. Below are the reports, with direct links, for anyone who wants to dig into the arguments and decision logic.

Aviva Investors House View

BNY Investments Vantage Point

Franklin Templeton Allocation Views

HSBC AM Investment Monthly

Invesco Uncommon Truths

JP Morgan Global Asset Allocation Views

OFI Asset Management Panorama

Pictet AM Barometer

Robeco Monthly Outlook

Russell Investments Asset Class Dashboard

Standard Chartered Global Market Outlook

T. Rowe Price Global Asset Allocation

The key takeaway for allocators

EM wins twice. That rarely happens because everyone suddenly falls in love with “EM” as a label. It usually happens because one macro regime supports two markets at once, USD direction, financial conditions, and broader growth beyond the US.

Market context: In 2025, EM equities delivered 35.06% in USD and 19.08% in EUR, almost identical to European equities at 35.54% in USD and 19.50% in EUR. That matters because the current EM preference is not simply a “catch-up trade” after weak performance. If anything, the consensus looks more like a regime call, with the USD and financial conditions as the common denominator, rather than a straightforward extrapolation of last year’s returns.

EM Equities

Why EM equities rank #1 despite a strong US

The core bull case for Emerging Markets Equities is simple, lower expectations, more upside asymmetry. The US is a strong runner-up, backed by earnings quality, scale, and AI leadership, but that strength also means the bar is high and there’s less room for positive surprises. EM is different, valuations embed less perfection, while a good enough macro backdrop, a stable or weaker USD, easier financial conditions, broader global growth and earnings outside the US, can translate disproportionately into EM earnings momentum and multiple expansion. For many allocators, EM becomes the more attractive risk/reward expression of risk-on, similar exposure, a lower price tag, and more upside if the macro picture cooperates.

53.1% overweight EM equities, what if the dollar turns?

Why skeptics say: “this isn’t cheap, it’s uncertain”

The bear case on Emerging Markets is straightforward, you’re not buying cheap, you’re buying uncertainty. The discount is a risk premium, because EM is vulnerable to a stronger dollar, higher US rates, and sudden risk-off episodes in which EM is often sold first. On top of that, EM is not one market, political risk, governance, capital controls, and geopolitical tensions, with China as a persistent shadow, can make returns highly volatile. In that worldview, investors prefer the US as quality risk-on and underweight EM.

Emerging Market Debt (EMD)

EMD ranks #1: carry wins, USD stays key

The bull case for Emerging Markets Debt is mainly a carry plus macro story. Many strategists see EMD as one of the few places in fixed income where compensation still feels meaningful, relatively high yields and attractive carry provide a built-in cushion. EMD also fits a backdrop in which the USD doesn’t strengthen, and ideally softens, acting as a tailwind, especially for local returns. In the same scenario, disinflation and firmer growth and fundamentals across parts of EM can stabilize the credit picture. If spreads are additionally supported by inflows and improving fundamentals, there’s not just carry, but also room for further spread tightening. This is why the consensus increasingly emphasizes selectivity, preferences such as hard currency and or IG sovereigns, where the risk/reward profile is often seen as cleaner.

The EMD skeptic: not “underweight,” but a conviction problem

In this set, the bear case for EMD is less an explicit underweight call and more a conviction problem, without a clear view on USD direction, spreads, and global risk appetite, EMD can quickly throw a portfolio out of balance. That shows up in more cautious framing, neutral on EM USD debt, not because carry is unattractive, but because timing the risk factors is hard. EMD can embed exposure to USD moves, spread volatility, and sentiment, meaning a risk-off shock or an unexpectedly strong dollar can erase the comfort of carry quickly. In that worldview, EMD is more of a balancing position than a high-conviction bet, staying selective, and scaling only when macro anchor points are aligned.

What this means for a tactical allocator

EM topping both markets signals the same thing, the consensus expects a regime in which USD headwinds fade and financial conditions don’t tighten sharply. That makes EM attractive, but also fragile, because the very same forces can support the trade or break it. Practically, a tactical allocator has two routes, embrace EM as the regime expression, with clear risk budgets and segment choices, hard vs local, IG vs HY, or treat EM as a position you must earn, only adding once your macro anchors are in place, USD, rates, risk appetite.

Debate this in the comments

Hot take: Overweighting EM Equities and EMD today is mostly a USD and financial-conditions call, more than a pure EM fundamentals call.

Where do you land?

A) Yes, it’s basically a dollar and conditions trade.

B) No, EM fundamentals and valuation/carry stand on their own.

Drop A or B below in “Discussion about this post”, then add one sentence: what’s your cut trigger, USD strength, higher US real yields, widening spreads, or a classic risk-off turn?