ASML Doubles. Your Gain: 0.30%

Most investors skip the most important question: how much of your portfolio is actually in equities?

Your portfolio holds 80% bonds, 15% equities and 5% ASML. ASML doubles. Your total return rises by 0.30%. Not because the calculation is right or wrong, but because allocation sets the ceiling. I see it time and again: investors who spend years searching for the next winner, whether that is ASML, Nvidia, or whatever name dominates the headlines, but have never asked how much of their capital is actually in equities. That question is more uncomfortable. And more important.

That sense of certainty has a name. In 1986, Brinson, Hood and Beebower showed in their study Determinants of Portfolio Performance (Financial Analysts Journal) that the vast majority of portfolio return variation is explained by asset allocation, not by the selection of individual securities. Not by timing. Not by finding the next winner. By the distribution. Forty years later, that conclusion has never been overturned.

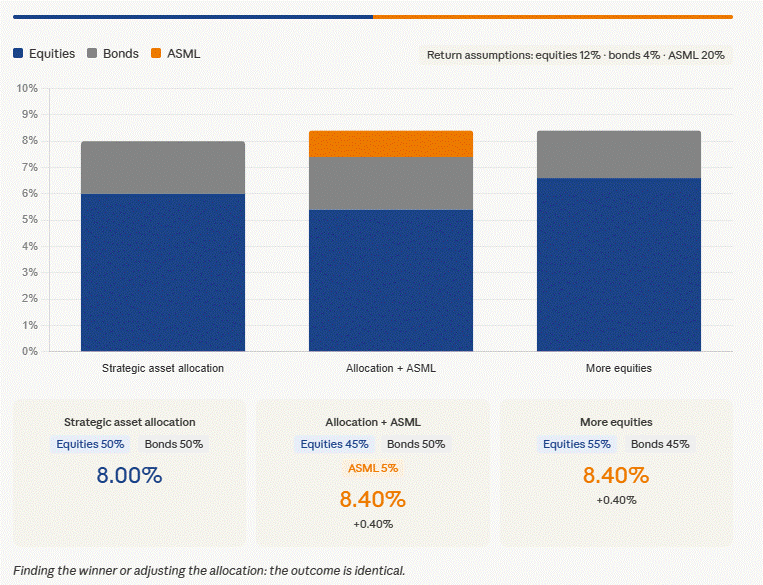

Here is what that 5% allocation is actually buying. The alternative was simple: hold 80% bonds and 20% equities broadly, with no single-stock position. That base allocation returns 5.60%. Adding the 5% ASML position lifts the total to 6.00%, a gain of 0.40 percentage points, but only because ASML doubled. If ASML had fallen 50% instead, that single position alone would have cost 2.5 percentage points, pulling the total return well below the base. The 0.40% gain is the price of taking concentration risk. It is not a free upgrade, and it is not available without the downside that comes with it.

And yet most investors start with the name, not the distribution.

The question is therefore not: which stock? The question is: how much are you actually in equities? And was that distribution a deliberate choice, or did it simply drift into place?

Those who start with the name skip the decision. Apple is always a safe bet. ASML can’t go wrong. The order is reversed. First the distribution, then the selection. Portfolio construction requires an honest conversation about objectives, time horizon and risk tolerance. That conversation is skipped too often.

I spoke with a young professional, sharp, driven, well educated. He said: “Honestly, I think asset allocation is a bit overrated. My advice is 100% equities. It always works out.” After Covid, it did indeed always work out. But the Asian crisis of 1998, the market crash of 1987, a bear market lasting five years: he had not lived through those. Not from books, but in a portfolio he was responsible for.

Experience is not interchangeable. Those who know these periods only from the literature have a different calibration than those who lived through them. That is not a criticism, it is a fact. The market teaches it to everyone eventually. Those who understand allocation are simply better prepared for the lesson.

A well-constructed portfolio feels redundant in a rising market. That is precisely why it matters.

New to this? Investing does not begin with choosing a stock, but with the distribution of your capital across different asset classes. That distribution, not the stock selection, determines the majority of what you ultimately earn.

The question was never which stock. The question was always how much.

Every month I read across 60+ asset manager reports. The distribution question is always the first one they answer. The Asset Allocation Report tracks where that consensus currently stands.