AI is everywhere in the portfolio — except where the decision is made

AI is reshaping every layer of the investment process. Except the one that decides how capital is allocated.

I spent six weeks looking for an investment committee that made an allocation decision based on AI output. I did not find one.

The filter

The research window ran from 1 March to 15 April 2026. The criteria were strict and cumulative: AI had to be embedded in the allocation decision itself, not in the research preceding it. The decision had to be owned by a CIO, head of asset allocation, or investment committee. And the implementation had to be live in an existing mandate — no pilots, no proofs of concept. No single case met all three conditions.

This is the second research round. The first window ran from January to February 2026, applying identical criteria. The outcome was the same.

Two rounds. Identical method. Identical result. That is not a single observation. That is a pattern forming.Zero cases. A clean result.

The near misses

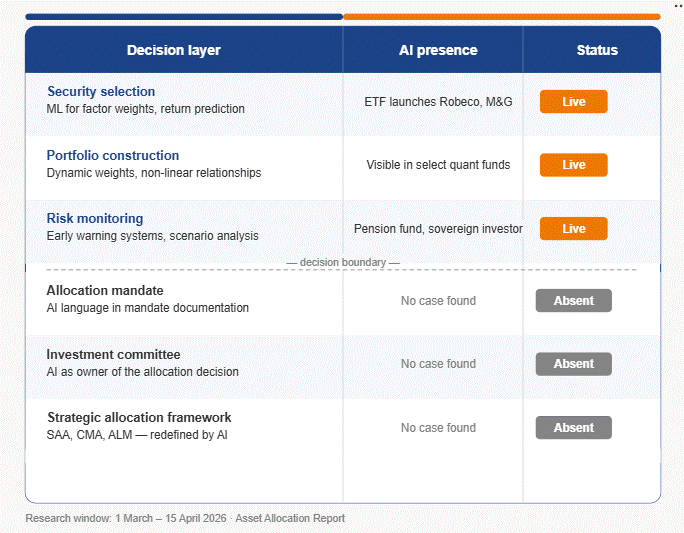

Several came close. A large pension fund embedded neural networks in scenario analysis and generated equity-buy signals during a stress period. A sovereign investor applied AI to improve predictive signals and tilt portfolios. A global asset owner used AI for risk monitoring and to support early divestment decisions.

These are not experiments. They are real implementations. But they sit one layer below allocation policy: they inform decisions, they do not make them.

Where AI is live

The contrast is sharpest in publicly listed strategies. Robeco launched the NextGen Global Small Cap ETF in March 2026, an active strategy using machine learning to detect non-linear relationships in return drivers and dynamically adjust signal weights at the level of individual stocks. M&G announced the Global Maxima Equity UCITS ETF in December 2025, built on a machine learning model trained on data from more than one thousand companies across twenty-five years.

Live portfolios. Trackable. Real. But they operate inside equity sleeves. They do not alter SAA frameworks. They do not revise capital market assumptions. They do not redefine allocation policy.

The decision boundary

AI is present in security selection, portfolio construction, and risk monitoring. Absent in allocation mandates, investment committee decisions, and strategic allocation frameworks. That boundary is not technical, it is institutional. An investment committee must be able to defend an allocation decision to a board, regulator, and client. That requires ownership: someone who puts their name to the answer. A model that autonomously determines what percentage goes to equities cannot provide that accountability. Until committees can delegate that responsibility, the decision remains human, regardless of the quality of the AI output.

The inputs are improving: better signals, sharper scenario analysis, more granular risk modelling. The decision itself has not yet shifted.

To change that, three things need to be visible: explicit AI integration in mandate language, adoption at investment committee level, and evidence of capital being reallocated as a direct result of AI output. None of these appeared in this window.

Result: no allocation impact found. Implementation expanding.

The boardroom is always last. In investment management, last is not a detail. Last is a decision.

New to this? Asset allocation is the decision that determines how much of a portfolio goes into equities, bonds, or other assets, and right now, that decision, the most consequential in the investment process, remains beyond the reach of AI.

AI is already used in investing, but the final decision on where money actually goes is still firmly human-led