3.39% Private Equity Premium, Structural Opportunity or Peak Optimism?

60 Capital Market Assumptions (CMA), 10-year nominal consensus, 9.75% Private Equity vs 6.36% Global Equities

This week’s Strategic Asset Allocation question

If expected returns keep drifting lower across asset classes, where does the long-term premium remain?

This year’s Expected Returns update shows 6.36% nominal for Global Equities over ten years. Private Equity stands at 9.75%.

The 3.39 percentage point gap looks compelling.

But does it reflect a durable liquidity premium or peak-cycle optimism?

One regime, two outcomes: Valuation pressure vs private market conviction

The 60 Capital Market Assumptions reports cluster around a 10-year horizon, average 11.1 years, nominal returns, mostly USD-based.

The direction is clear. Expected returns continue to compress, especially in public equities. Inflation supports nominal figures, yet elevated valuations constrain future premia.

Private Equity retains a meaningful premium in forward estimates. The consensus clusters around 9.8%, signaling conviction.

The regime remains consistent, slower growth, higher rates, tighter liquidity. Yet outcome expectations diverge.

At a glance

60 CMA reports, record sample size

Average forecast horizon 11.1 years, median 10 years

Global Equities 10-year nominal consensus 6.36%

Private Equity 10-year nominal consensus 9.75%

Implied Private Equity premium 3.39 percentage points

EUR hedged adjustment about minus 1.10% annually over ten years

10-Year Nominal Expected Returns (USD)

Three observations matter.

First, consensus, median, and middle quintile align in both assets. The crowd shows internal coherence.

Second, dispersion in Private Equity exceeds that of public markets. The uncertainty band runs wider.

Third, the 3.39% premium surpasses long-term realized differentials.

The key takeaway for allocators

The consensus holds steady. The premium remains elevated. The uncertainty exceeds the headline figure.

In Strategic Asset Allocation (SAA) and Asset Liability Management (ALM) frameworks, dispersion and currency treatment may outweigh the point estimate.

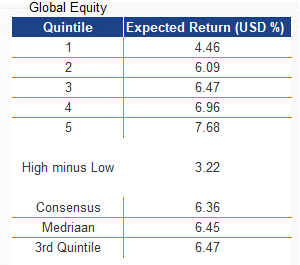

Global Equities

6.36% Expected Return, 60 Managers, Why Valuations Cap the Upside

The 10-year nominal consensus for Global Equities stands at 6.36%. Median and middle quintile cluster near 6.45%.

This reflects a balanced building-block view. Inflation supports nominal returns, yet starting valuations limit forward premia. Recent quarters show continued downgrades, averaging minus 0.15 percentage points.

The assumption favors normalization over expansion. Lower multiples and moderate earnings growth shape the outlook.

3.22% Dispersion, Why Scenario Risk Dominates

The gap between the highest and lowest quintile reaches 3.22 percentage points. That spread influences ALM outcomes.

If inflation surprises upward or real yields remain elevated, valuation compression could persist. If productivity accelerates, multiples may stabilize. Path dependency defines the risk.

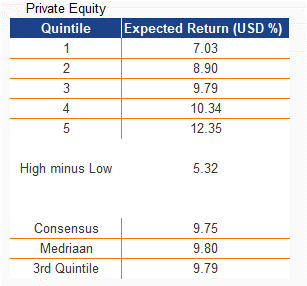

Private Equity

9.75% Expected Return, 3.39% Premium, Why the Liquidity Story Persists

Private Equity consensus stands at 9.75% nominal over ten years. Median and middle quintile align near 9.8%.

The implied premium over Global Equities equals 3.39 percentage points. In 2015, the gap measured 2.63%. It widened again in 2024 and remains elevated.

Supporters cite operational value creation, pricing power, and long-duration capital. Infrastructure and private markets also offer partial inflation linkage.

5.32% Dispersion, Why Liquidity Assumptions Deserve Scrutiny

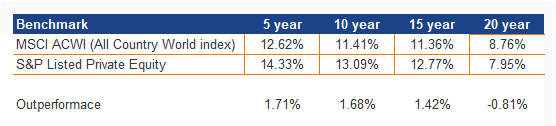

The spread between the highest and lowest quintiles is 5.32 percentage points. This uncertainty points to uncertainty among strategists and CIOs when making capital market assumptions. Perhaps prompted by actual returns, the table below shows the difference between the MSCI ACWI and the S&P Listed Private Equity index over the past 20 years.

The 3.39% expected premium presumes orderly refinancing, stable leverage, and functioning exit markets. Recent cases such as Accell show that even experienced sponsors misjudge operating risk when growth stalls.

Stress rarely starts in liquid markets. It often surfaces first where pricing is opaque and transactions freeze. Redemption gates in private credit funds illustrate how promised liquidity can collide with illiquid underlying loans.

If exit multiples compress and refinancing costs remain elevated, the projected premium narrows quickly. The premium may be real. But it only holds if liquidity holds.

What this means for a strategic allocator

Private Equity does not serve Tactical Asset Allocation (TAA), yet its forward premium shapes strategic risk budgets. If the 3.39% differential compresses toward historical norms, portfolio efficiency assumptions weaken.

Debate this in the comments

A) The 3.39% Private Equity premium reflects structural compensation for illiquidity.

B) The premium will revert toward 1 to 1.5%, pressuring strategic return targets.

Which side do you support, and why?