14% Overweight Government Bonds in 72 TAA Reports, Why the Minority Also Backs Equities

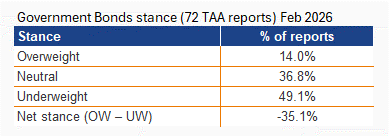

In this month’s consensus, only 14.0% are Overweight Government Bonds (vs 36.8% Neutral, 49.1% Underweight). Still, a distinct minority within 72 TAA reports combines an Overweight in Government Bonds

This week’s Tactical Asset Allocation question

When nearly half of strategists underweight an asset class, does that make it wrong, or simply unloved?

Across 72 Tactical Asset Allocation (TAA) reports, Government Bonds rank last within Fixed Income. Yet 14% still hold an overweight. That minority is not random. It follows a distinct playbook across bonds and equities.

Source: Alpha Research - Asset Allocation Consensus February 2026

The real question is not whether Government Bonds are cheap. It is what role they play in a portfolio.

One regime, two outcomes: Hedge duration versus carry conviction

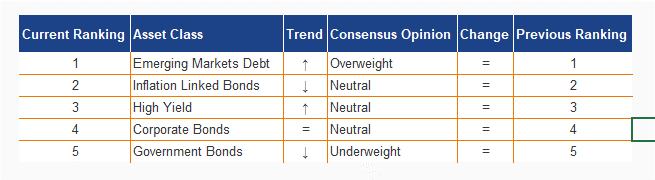

Fixed Income splits into two camps. The consensus prefers Emerging Markets Debt (EMD). It leans on carry, spread compression, and a weaker US dollar.

Source: Alpha Research - Asset Allocation Consensus February 2026

The Government Bonds minority sees a different regime. In their framework, duration regains value as ballast. Term premia and steeper curves offer carry and roll down. They also argue for selectivity, not broad exposure.

These views rarely coexist in one portfolio. This is not a bond debate. It is a portfolio design debate.

At a glance

Sample: 72 active Tactical Asset Allocation (TAA) reports, data through 31 January 2026

Government Bonds stance: 14.0% overweight, 36.8% neutral, 49.1% underweight

Government Bonds are the least preferred Fixed Income segment in the sample

100% of Government Bond bulls are also overweight equities

The consensus Fixed Income preference remains Emerging Markets Debt (EMD)

Government Bonds versus EMD: the Fixed Income split

Government Bonds sit at the bottom of the Fixed Income preference list. Emerging Markets Debt sits at the top. Inflation Linked Bonds and High Yield also rank ahead of Government Bonds in the consensus.

That ranking matters because the choice is rarely additive. In practice, a Government Bonds overweight often means less room for EMD.

The key takeaway (for allocators)

The Government Bonds bulls are not running a classic defensive book. They pair duration exposure with overweight equities. The disagreement is not about safety. It is about structure.

Government Bonds

4 drivers the bulls cite, why duration is back

The bull case rests on four pillars.

First, the hedge role. Treasuries and other developed market government bonds can still cushion downside growth shocks, according to UBS and BlackRock.

Second, compensation is improving. Wellington highlights term premia and steeper curves, which can deliver carry and roll down.

Third, they emphasize geography. BlackRock prefers developed market government bonds outside the US. Franklin Templeton and UBS see value in UK Gilts. Morgan Stanley points to opportunities in European peripherals.

Fourth, they treat duration as stabilizer, not a substitute. They keep equities overweight and use Government Bonds to shape drawdown behavior.

4 headwinds the bears stress, why fiscal risk dominates

The bear case is also coherent.

First, valuation looks thin. Nuveen and Schroders describe government bonds as offering little value.

Second, fiscal dynamics matter. Pictet, Invesco, SEB, and Société Générale warn that rising deficits and heavier issuance can push yields higher.

Third, rate cuts may not save duration. UniCredit and VP Bank flag scenarios where yields rise despite easing.

Fourth, core markets face specific skepticism. UBS is underweight Bunds, and Morgan Stanley is cautious on core government bonds.

Emerging Markets Debt (EMD)

5 reasons EMD leads the consensus, why carry wins

EMD remains the preferred bond segment in the consensus.

The case starts with yield. Several managers cite attractive carry as the base return engine, including Nuveen, T. Rowe Price, and UBP.

The second leg is currency. Franklin Templeton and UBP highlight a weaker US dollar as a tailwind for returns, especially in local markets.

Third, fundamentals look supportive. Franklin Templeton and Pictet point to disinflation and better growth dynamics across parts of emerging markets.

Fourth, spreads can help. JP Morgan, PineBridge, and Morgan Stanley argue that inflows and fundamentals can support tighter spreads.

Fifth, the allocation is selective. Morgan Stanley and UOB Asset Management (UOB AM) prefer hard currency exposure and higher quality sovereigns.

The bear case is muted, why neutrality still matters

Explicit underweight calls are scarce in this dataset. The main caution is a neutral stance on EM US dollar debt from BNY, framed as balance rather than conviction.

That silence does not remove risk. EMD can suffer if the US dollar strengthens, spreads widen, or geopolitics disrupt flows.

What this means for a tactical allocator

Start with intent. If you want Fixed Income to hedge macro downside, Government Bonds can fit. If you want Fixed Income to earn carry, EMD fits more naturally.

Then stress test the fiscal backdrop. If you expect deficits and issuance to keep term premia elevated, duration will behave differently than in prior cycles.

Finally, note the profile signal. The Government Bonds minority also runs overweight equities. They are not retreating from risk. They are building a portfolio with two engines and a stabilizer.

Debate this in the comments

A) Government Bonds are a renewed hedge inside an equity overweight portfolio

B) Government Bonds are structurally impaired under fiscal dominance

What single macro development would make you change your duration stance?