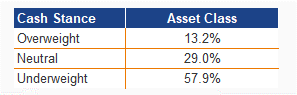

13.2% Overweight Cash, what do these contrarians see?

In this month’s consensus, only 13.2% are Overweight Cash (vs 29.0% Neutral, 57.9% Underweight). Still, there is a small subgroup of 5 asset managers that is 100% Overweight Cash.

This week’s question

Cash is supposed to be the least interesting line in the portfolio, and right now it still is, but what are the contrarians thinking? Most CIOs and strategists see cash as the least attractive asset class, and the consensus percentages are clear. Yet a small minority chooses the opposite. So the real question is not whether cash is “good” or “bad”. This week’s question is: what kind of allocator goes Overweight Cash, and where does that profile diverge most sharply from the crowd?

One regime, two outcomes: Overweight Cash is not “less risk”, it is “different risk”

The analysis shows that allocators who are Overweight Cash do not suddenly turn bearish on equities. They keep equities firmly Overweight, in line with the consensus. The big divergence shows up elsewhere: bonds move from Underweight in the consensus to maximum Underweight in the contrarian profile. What does not go into duration stays liquid in cash. And within fixed income, the profile becomes more selective and more assertive: less government duration, more spread and EM carry. The end result looks like a barbell: safety via cash, return seeking via High Yield and Emerging Market Debt, while classic government bond duration is consciously avoided.

At a glance

Cash positioning in the full sample: 13.2% OW, 29.0% Neutral, 57.9% UW

The contrarian subgroup consists of 5 asset managers, all 100% OW Cash

Their top level profile: OW Equities, heavy UW Bonds, OW Cash

Within fixed income: UW Government Bonds (sharp), UW Inflation Linked, UW Corporate, but OW High Yield and OW Emerging Market Debt

Regional equity tilts: more positive than the consensus on Japan and Emerging Markets

Practical interpretation: this is primarily a duration avoidance stance, not a generic risk off posture

Cash: consensus percentages, plus the contrarian filter

1) Cash positioning in the full sample

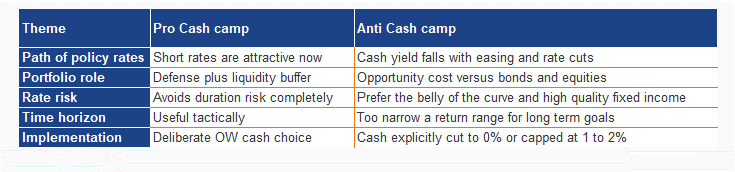

2) Decision map: what the camps truly disagree on

Sources behind the contrarian cash profile

Franklin Templeton Allocation Views

Northern Trust AM Investment Perspective

Russell Investments Asset Class Dashboard

T. Rowe Price Global Asset Allocation

VP Bank Our View

The key takeaway for allocators

Overweight Cash is not “lazy parking”. In this dataset it is a structured duration decision: the contrarians diverge on bonds, not on equities. They keep equity risk, avoid government duration, and then hunt income via High Yield and Emerging Market Debt, while cash functions as ballast and optionality.

Cash

4 reasons why Cash works now: yield, defense, and dry powder

The pro cash case is about function. Cash is a shock absorber and keeps optionality alive when markets dislocate. With elevated short term rates, cash can feel like a rare “risk free” return stream, especially for allocators who want to avoid the volatility of longer duration bonds. Cash can also be framed as readiness: liquidity to seize opportunities when markets dislocate, rather than a strategic end state. In that view, Overweight Cash is not doing nothing, it is buying flexibility while still earning carry.

4 reasons why Cash may disappoint later: cuts, opportunity cost, and weak compounding

The anti cash case is simple and sharp. If policy eases, cash yield reprices down quickly. What looks attractive today can become a narrow return range that struggles to meet long term goals. Opportunity cost is the second hit: if intermediate duration and high quality fixed income offer a better entry point and a better risk adjusted return, then staying in cash becomes expensive. That is why several allocators push cash explicitly lower in their models, sometimes toward zero, forcing the portfolio to earn returns elsewhere.

Bonds (Fixed Income)

3 reasons why bonds are the real battleground: duration is the red flag (the OW Cash profile)

This Overweight Cash analysis shows that the main divergence is not in equities, but in duration. This contrarian subgroup agrees with the consensus that government bonds are unattractive, but with maximum conviction. There is also less appetite for inflation linked and corporate bonds, where the consensus is closer to neutral. This suggests these tactical allocators believe the portfolio is not being paid sufficiently for rate risk. Cash then becomes the alternative to duration, not a replacement for risk assets overall.

3 reasons why the barbell can still be fragile: credit and EM risk can bite hard (the same OW Cash profile)

The twist is that these allocators do not simply take less risk, they relocate it. By overweighting High Yield and Emerging Market Debt, they reintroduce cyclical and liquidity risk through spreads. In a regime where growth disappoints or spreads widen, HY and EMD can sell off sharply. Cash helps as a stabilizer, but it does not hedge spread blowouts. That is why the profile reads as a barbell: safety in cash, income and return seeking in HY and EMD, and minimal exposure to government duration in the middle.

What does this mean for a tactical allocator

See Overweight Cash as a signal about rates, not as a generic risk off label. In this dataset, the contrarian allocator says: keep equities, cut duration hard, hold cash, and earn carry via HY and EMD. If your base case is easing without a spread shock, that structure can work. If your risk case is widening spreads or EM stress, the barbell can wobble, even with a large cash anchor.

Debate this in the comments

A) Overweight Cash is the cleanest hedge against duration risk, and the HY plus EMD barbell is the right compromise.

B) Overweight Cash is a temporary illusion, if you fear duration, you should own high quality bonds, not replace bonds with cash.

Pick A or B and name one trigger that would make you switch sides (first cut, curve steepening, widening spreads, or an equity drawdown).